The Short Answer:

Yes—but only if you price and position your home correctly for today’s market.

Rhode Island is still experiencing limited inventory, steady buyer demand, and price resilience. However, today’s buyers are more selective than they were just a few years ago. That means strategy matters more than timing.

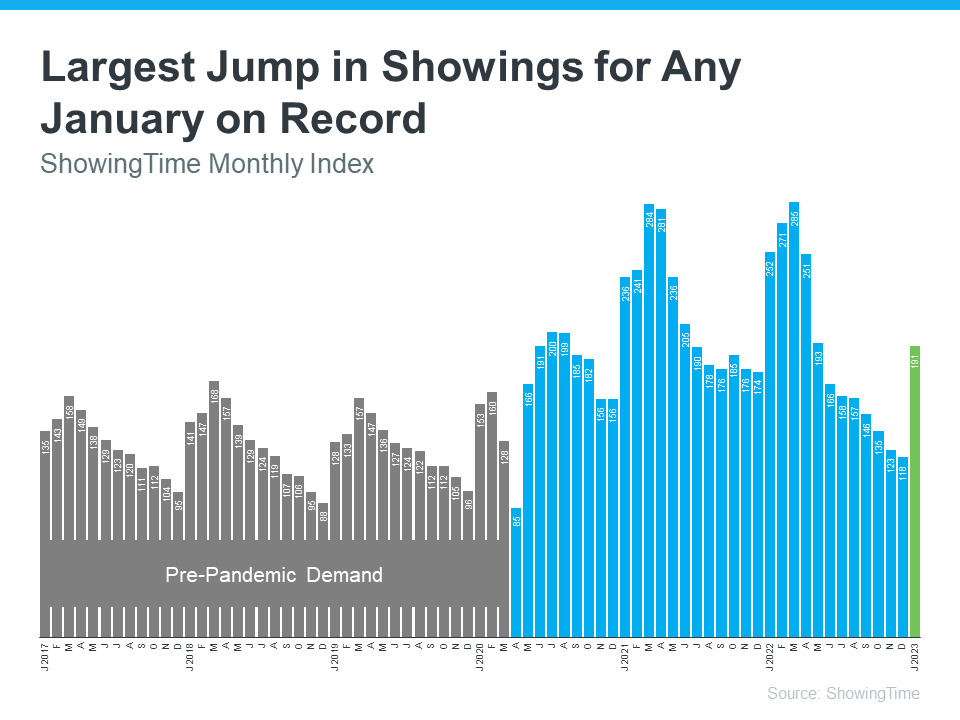

📊 What’s Happening in the Rhode Island Housing Market Right Now?

The 2026 market is defined by three key factors:

1. Low Inventory Still Favors Sellers

There are still fewer homes available than buyers actively searching—especially in Northern Rhode Island communities.

2. Buyers Are More Price-Sensitive

Higher mortgage rates have changed buyer behavior. Today’s buyers are:

- More cautious

- More analytical

- Less willing to overpay

3. Well-Priced Homes Are Still Selling Quickly

Homes that are priced correctly—and marketed strategically—are still attracting strong interest and, in many cases, multiple offers.

🤔 Should You Sell Now or Wait?

You Should Consider Selling Now If:

- You’ve built significant equity

- Your home fits what buyers are actively looking for

- You’re planning a move within the next 6–12 months

- You want to maximize value before more inventory enters the market

You May Want to Wait If:

- Your home needs major updates

- You’re unsure about your next move

- You’re expecting major local market changes (rare, but possible)

💡 The Biggest Mistake Sellers Are Making Right Now

The #1 mistake I’m seeing:

👉 Pricing based on last year’s market instead of today’s market

What worked in 2021–2022 does NOT work the same way today.

Overpricing leads to:

- Fewer showings

- Longer days on market

- Price reductions

- Lower final sale price

🧠 The Luca Method: How Smart Sellers Win in Today’s Market

This is where strategy separates results.

As part of The Luca Method, I focus on:

✅ Strategic Market Intelligence

Understanding real-time buyer behavior—not headlines

✅ Positioning Your Home to Attract Demand

Pricing, presentation, and exposure all working together

✅ Creating Competition (Not Just Listing a Home)

The goal is not just to sell—it’s to maximize your outcome

📥 Free Download: Rhode Island Home Value Strategy Guide

If you’re even thinking about selling, this is the first step.

👉 Receive my Rhode Island Home Value Strategy Guide

Learn:

- How to price your home correctly in today’s market

- What buyers are really looking for right now

- How to avoid the mistakes that cost sellers thousands

📩 Send an email to Joe@JoeLucaRealtor.com with Home Value Strategy as the subject.

🔗 Related Articles You Should Read Next

To help you go deeper, I recommend:

- “How to Price Your Home to Sell in Today’s Market”

- “Why Overpricing Your Home Can Cost You Money”

- “Understanding Buyer Behavior in a Changing Market”

(These topics are all connected—and understanding them together gives you a major advantage.)

📞 Thinking About Selling? Let’s Talk Strategy

If you’re considering selling—even if it’s 6–12 months away—the best move is to start with a conversation.

📲 Call/Text: 401-409-5030

📧 Email: Joe@JoeLucaRealtor.com

Final Thought

You don’t need to “time the market” perfectly.

👉 You need a strategy that works in the market you’re in.

And that’s exactly what I help my clients do every day.