There are lots of headlines, and posts on social media trying to “scare” people about the real estate market.

But remember this, Real Estate has been vote “The Best Investment” EIGHT Years in a row.

The reasons are simple supply and demand. There are more buyers than sellers. In fact, our housing supply is 5.2 million units short of demand. Think about that. It could take ten years for supply to match demand.

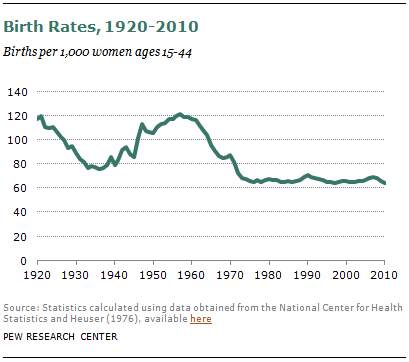

How do we know that demand is sustainable? As can be seen in the image from the Pew Research Center, US birth rates in the 1970’s through 2010, have been largely flat. So the US demand for housing should remain strong. Also bear in mind that rental rates have been increasing as much as 19%/year in many areas. With mortgage interest rates at or below HALF of the historic average for a 30 year fixed rate mortgage (8%,) many Renters may make the decision too pay their own mortgage, and not their Landlord’s mortgage.

“But, is now a good time to sell MY house?”

Before COVID, if you sold your house and purchased another house, assuming only an annual rate of 10% equity accumulation, you would now have over 20% additional equity in the home you bought two years ago.

We may not continue that rate of equity accumulation, but it does provide legitimate evidence that now is a good time to sell AND a good time to buy a home.

Call or text 401-232-4300 for answers to your real estate questions.

The Path To Homeownership Can Be Steeper for Some Americans

As we celebrate Black History Month, we honor and recognize the past and present experiences of Black Americans. A significant part of this experience is investing in a home of their own. While equitable access to housing has come a long way, the path to homeownership is still steeper for households of color. It’s an important experience to talk about, along with how working with the right real estate experts can make all the difference for diverse homebuyers.

We know it’s a more challenging journey to achieve homeownership for some because there’s still a measurable gap between the overall average U.S. homeownership rate and that of non-white groups. Today, the lowest homeownership rate persists in the Black community (see graph below):

Homeownership is an essential piece for building household wealth that can be passed down to future generations. However, there are obstacles in the homebuying process that can negatively impact certain racial and ethnic groups, including the Black community. This can delay or prevent many from achieving homeownership, challenging their ability to grow their net worth. A report by Vanessa G. Perry of the George Washington University School of Business and Janneke Ratcliffe of the Urban Institute explains:

“. . . households of color have much lower homeownership rates than white households and consequently hold, at the median, just one-eighth the wealth of white households.”

On top of that, when Black households do become homeowners, research shows they pay more for those homes overall than the average household. Raheem Hanifa, a Research Analyst for the Joint Center for Housing Studies of Harvard University, tells us:

“Black homeowners not only have primary mortgages with higher interest rates than white homeowners with similar incomes, they also have higher interest rates than white homeowners with substantially lower incomes, . . . Black homeowners have experienced systemic barriers to homeownership and wealth-building opportunities that have limited their ability to access credit, which is a key component in receiving low mortgage interest rates.”

For Black homebuyers, the inequity that remains in housing can be a point of pain and frustration. That’s why it’s so important for members of diverse groups to have the right team of experts on their sides throughout the homebuying process. These professionals aren’t only experienced advisors who understand the market and give the best advice. They’re also compassionate allies who will advocate for your best interests every step of the way.

Bottom Line

Opportunities in real estate improve every day, but there are still equity challenges that many face. Let’s connect to make sure you have an advocate on your side as you walk the path to homeownership.

Many members of Generation Z (Gen Z) are aging into adulthood and deciding whether to rent or buy a home. If you find yourself in this group, it’s important to understand you’re never too young to start thinking about homeownership. The sooner you start planning, the sooner you can move on from renting.

As you set off on your journey and plan your next move, here are a few reasons to think about homebuying this year.

The Reasons Gen Z Want To Become Homeowners

While the majority of Gen Z haven’t entered the housing market yet, a large portion plan to according to a realtor.comreport. The report found that 72% of Gen Z would rather purchase a home than rent long-term. As George Ratiu, Manager of Economic Research for realtor.com,says:

“With nearly three-quarters of those surveyed preferring to buy versus renting long-term, the housing industry should be prepared for millions of Gen Z buyers to bring a new wave of demand along a similar stage-of-life timeline as the millennial generation before them.”

But why do so many members of Gen Z value homeownership? According to the latest Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), young homebuyers – more than any other age group – want to become homeowners because they want to have a place of their very own.

That may be because one of the biggest benefits of homeownership is having a place that you can truly make your own by customizing it to your style and personality. Whether that’s the décor, painting, or renovations, when you own your home, you don’t have to limit yourself to what your lease and landlord will allow.

Not to mention, owning a home provides much greater long-term stability and security than renting. When you own a home, there’s also protection from steadily rising rental costs because your monthly mortgage payment is locked in for the length of your loan (typically 15 to 30 years).

Work with a Real Estate Professional To Achieve Your Goals

Whether you’re just getting started on your homebuying journey, you want to learn more about the process, or you’re fully committed to buying your first home this year, it’s especially important to connect with a trusted real estate advisor soon, as you won’t be the only first-time buyer in the market. According to a recent survey from realtor.com, a majority of first-time buyers surveyed are looking to purchase a home in 2022. As the survey notes:

“First-time home buyers retain their optimism despite a challenging housing market in the past year. Hoping to achieve their goal of homeownership and provide a comfortable space for their families, young buyers are setting out to learn what they can about the market and setting their list of priorities for their home purchase.”

That means you’ll likely face strong competition from other first-time buyers. One way to get a leg-up on that competition is to work with a real estate professional to make sure you have the support you need to make an informed and confident decision.

Bottom Line

If you’re planning your next move, you’re not alone. Just know it’s never too early to consider the benefits of homeownership over renting. To learn more, let’s connect today so you have a trusted professional on your side to help you explore your options.

Over the past two years, we’ve lived through one of the most stressful periods in recent history. Because of the health crisis, many of us have spent more time at home and that’s led us to re-evaluate both what we need in a house and how much we appreciate having a safe space. If you’ve found your current home isn’t filling all your needs, you may be wondering if it’s time to find a new one.

There’s reason to believe a change of scenery could boost your happiness. Catherine Hartley, an Assistant Professor at New York University’s Department of Psychology and co-author of a study on how new experiences impact happiness, says:

“Our results suggest that people feel happier when they have more variety in their daily routines—when they go to novel places and have a wider array of experiences.”

A move could be exactly the new experience you’ve been looking for. If that’s something you’re considering to better your lifestyle, here are a few things to keep in mind.

Approach Your Decision Thoughtfully and Explore Your Options

Buying and selling a home is a major life change, and it’s not a decision you should enter lightly. But, if you’re questioning whether or not a move would bring you more happiness, it’s important to explore if it’s the right choice for you.

To find out more and discuss your options, reach out to a local real estate professional. They’ll explain the process – including how to list your existing house and search for a new one – in clear and simple terms.

You should also think about your lifestyle and what you’re hoping to get out of your move. What needs aren’t being met in your current home? What features would bring you more joy and make your life easier? For example, are you now working remotely and need a home office? Do you crave more fresh air and open outdoor space to unwind in? Knowing the answers to these questions can help you get started and position your real estate advisor to work with you so you can find just the right home.

Consider a Location with Weather That Will Boost Your Mood

Home features aren’t the only thing to consider. You should also weigh your options when it comes to location. Is the weather something that’s important to you? Does it have a tendency to impact your mood? If it does, you may want to factor it into your next move. The World Population Reviewshares:

“What states have the best weather? When evaluating each state for temperature, rain, and sun, some states stand out. . . . Climate and weather preferences are personal and subjective. . . . “

Better weather can mean different things to different people. Some prefer the heat, others cooler temperatures, and some want to experience all four seasons. Think about what makes you feel happiest and prioritize that in your home search. If you’re moving to a whole new location, your agent is a great resource with a strong network to support you along the way.

Bottom Line

Moving could provide you with a fresh beginning and the chance to find happiness in your new home. Let’s connect today to talk about your goals and options in the current market.

You may have heard that it’s important to get pre-approved for a mortgage at the beginning of the homebuying process, but what does that really mean, and why is it so important? Especially in today’s market, with rising home prices and high buyer competition, it’s crucial to have a pre-approval letter prior to making an offer. Here’s why.

Being intentional and competitive are musts when buying a home this year. Pre-approval from a lender is the only way to know your true price range and how much money you can borrow for your loan. Just as important, being able to present a pre-approval letter shows sellers you’re a qualified buyer, something that can really help you land your dream home in an ultra-competitive market.

With limited housing inventory, there are many more buyers active in the market than there are sellers, and that’s creating some serious competition. According to the National Association of Realtors (NAR), homes today are receiving an average of 3.8 offers for sellers to consider. As a result, bidding wars are still common. Pre-approval gives you an advantage if you get into a multiple-offer scenario, and these days, it’s likely you will. When a seller knows you’re qualified to buy the home, you’re in a better position to potentially win the bidding war.

“By having a pre-approval letter from your lender, you’re telling the seller that you’re a serious buyer, and you’ve been pre-approved for a mortgage by your lender for a specific dollar amount. In a true bidding war, your offer will likely get dropped if you don’t already have one.”

Every step you can take to gain an advantage as a buyer is crucial when today’s market is constantly changing. Interest rates are rising, prices are going up, and lending institutions are regularly updating their standards. You’re going to need guidance to navigate these waters, so it’s important to have a team of professionals such as a loan officer and a trusted real estate advisor making sure you take the right steps and can show your qualifications as a buyer when you find a home to purchase.

Bottom Line

In a competitive market with low inventory, a pre-approval letter is a game-changing piece of the homebuying process. Not only does being pre-approved bring clarity to your homebuying budget, but it shows sellers how serious you are about purchasing a home.

Homeownership has long been considered the American Dream, and it’s one every American should feel confident and powerful pursuing. But owning a home is also a deeply personal dream. Our home provides us with safety and security, and it’s a place where we can grow and flourish.

Today, we remember the legacy of Dr. Martin Luther King, Jr. Many of us will remember his passion and determination for the causes he championed, including his famous “I Have a Dream” speech in 1963. As we reflect on his message today, it may inspire your own dream of homeownership. And if so, know you’re not alone. With a trusted real estate advisor at your side, you can begin your journey toward homeownership by answering the questions below.

1. Where Do I Start?

The process of buying a home is not one to enter into lightly. You need to decide on key things like how long you plan on living in an area, how much space you need, what kind of commute works for you, and how much you can spend.

Then, when you decide you’re ready to buy, you’ll need to apply for a mortgage. Your lender will look at several factors to determine how much you’re able to borrow, including your credit history. Lenders want to understand how well you’ve managed paying your student loans, credit cards, car loans, and other past debts.

“To get a rough estimate of what you can afford, most lenders suggest that you should spend no more than 28% of your monthly gross (pre-tax) income on your mortgage payment, including principal, interest, taxes and insurance.”

2. How Do I Save Enough for a Down Payment?

Speaking of how much you can afford, you’ll want to know what to save for a down payment. While the idea of saving for a down payment can be daunting, there are many different options and resources that can help.

According to Business Insider, automatic savings can bring you one step closer to achieving your target down payment:

“If you receive your paycheck as a direct deposit, you may want to arrange for your company to send a percentage of each check directly into a savings account for the down payment. . . . The automatic-savings strategy makes it so you don’t have to constantly remember to save money.”

Before you know it, you’ll have enough for a down payment if you’re disciplined and thoughtful about your process. And the best part is, you may need to save less for your down payment than you think. Your agent and lender can help you understand your options.

3. How Can I Reach My Financial Goals?

Another way to increase your savings is by sticking to a planned budget. If you’ve never budgeted before, there are tools available. For example, MoneyFit.org provides a budgeting worksheet you can use to create your own plan and five rules to follow when you’re saving. They recommend you:

Identify Goals

Record Expenses

Record Earnings

Compare and Calculate

Fix Weak Spots

If you’re already budgeting, consider finding ways to tighten your spending a bit more to accelerate your journey to homeownership. After all, putting even a little extra into your savings each month can truly add up over time.

Bottom Line

As you set out to realize your dream of homeownership this year, know that it’s achievable with careful planning. Most importantly, let’s connect today so you don’t have to walk alone on this journey.

If your goal is to purchase a home this year, you might be looking for any advantage you can get in today’s sellers’ market. While competition is still fierce for homebuyers, there are ways you can win and secure the home of your dreams, even in a hot market.

Father and son laughing and playing in the park together

Act Early and Save

The earlier you act this year, the more affordable your purchase will be. That’s because experts project mortgage rates will rise as we move deeper into 2022. According to Freddie Mac, the average 30-year fixed-rate mortgage is expected to be 3.5% by year’s end. Experts forecast home prices will rise as well.

That means the longer you wait, the more it will cost you to buy a home. Instead, act early and purchase your home before rates and prices rise further. Not to mention, the sooner you buy, the sooner you can experience the benefits of continued home price appreciation yourself. Once you have your home, you’ll be able to watch its value rise, giving you confidence that your investment is a sound one.

Buy Now, Move Later

Keep in mind, with high buyer demand like we’re seeing today, you’ll be competing against other potential homebuyers, which means you need to find a way to stand out. One way to accomplish this is to negotiate with sellers and present terms that meet their ideal needs. Danielle Hale, Chief Economist for realtor.com, explains one lever flexible buyers can pull to entice sellers:

“For buyers with more flexible timelines – such as those making a move from a big city – offering a couple extra months on the closing date could sweeten the deal for sellers who also need to buy their next home.”

In other words, if you’re eager to purchase a home now before it becomes more costly and you don’t have to move right away, you could extend the date of your closing and provide the seller with the time they need to find their next home. That’s a deal that could benefit both parties and help you stand out from the crowd.

Of course, it’s important to work with a real estate professional for expert advice on how to make your best offer. Your trusted advisor knows what’s working in your market and what may appeal to sellers.

Bottom Line

Experts project home prices and rates will increase in 2022. That means buyers who are ready should act soon and find ways to strengthen their offer to meet sellers’ needs. Let’s connect today to learn how you can win in today’s market.

It’s economy 101 – when supply is low and demand is high, prices naturally rise. That’s what’s happening in today’s housing market. Home prices are appreciating at near-historic rates, and that’s creating some challenges when it comes to home appraisals.

In recent months, it’s become increasingly common for an appraisal to come in below the contract price on the house. Shawn Telford, Chief Appraiser for CoreLogic, explains it like this:

“Recently, we observed buyers paying prices above listing price and higher than the market data available to appraisers can support. This difference is known as ‘the appraisal gap . . . .’”

Why does an appraisal gap happen?

Basically, with the heightened buyer demand, purchasers are often willing to pay over asking to secure the home of their dreams. If you’ve ever toured a house you’ve fallen in love with, you understand. Once you start to picture yourself and your furniture in the rooms, you want to do everything you can to land the property, including putting in a high offer to try to beat out other would-be buyers.

When the appraiser comes in, they look at things a bit more objectively. Their job is to assess the inherent value of the home, so they’re going to study the facts. Dustin Harris, Appraiser Coach, drives this point home:

“It’s important for everyone to understand that the appraiser’s job in the end is to remain that unbiased third party, to truly tell the client what that home is worth in the current market, regardless of what decisions have been made on the price side of things.”

In simple terms, while homebuyers may be willing to pay more, appraisers are there to assess the market value of the home. Their goal is to make sure the lender isn’t loaning more money than the home is worth. It’s objective, rather than emotional.

In a highly competitive market like today’s, having a discrepancy between the two numbers isn’t unusual. Here’s a look at the increasing rate of appraisal gaps, according to data from CoreLogic (see graph below):

What does this mean for you?

Ultimately, knowledge is power. The best thing you can do is understand appraisal gaps may impact your transaction if you’re buying or selling. If you do encounter an appraisal below your contract price, know that in today’s sellers’ market, the most common approach is for the seller to ask the buyer to make up the difference in price. Buyers, be prepared to bring extra money to the table if you really want the home.

Above all else, lean on your real estate agent. Whether you’re a buyer or seller, your trusted advisor is your ally if you come up against an appraisal gap. We’ll help you understand your options and handle any additional negotiations that need to happen.

Bottom Line

In today’s real estate market, it’s important to stay informed on the latest trends. Let’s connect so you have an ally to help you navigate an appraisal gap to get the best possible outcome.

In the maze of forms, financing, inspections, marketing, pricing, and negotiating, it makes sense to work with professionals who know the community and much more. It is always best to use an Experienced local REALTOR® who serves your area. The REALTOR® is the “Hub” of the transaction and will refer clients to the best lenders, home inspectors, closing/escrow companies, and moving companies. A good REALTOR® will know who is experienced, professional, licensed (when necessary), insured and provides great service to his/her clients.

2. Get a Mortgage Pre-Approval

Most first-time buyers need to finance their home purchase, and a consultation with a preferred mortgage lender is a crucial step in the process. Find out how much you can afford before you begin your home search. You will need a mortgage pre-approval before you can submit an Offer; we will show you homes as soon as you receive a pre-approval. **In Fact, due to COVID many Sellers instruct listing agents to only show their home to individuals that are pre-approved for a mortgage.

Get the Right Mortgage for Your Situation

There are many different types of mortgage programs out there, but as a first-time home buyer, you should be aware of the three basics: adjustable rate, fixed rate and interest-only.

Adjustable rate mortgages (ARMs) are short-term mortgages that offer an interest rate that is fixed for a short period, usually between one to seven years. After that, the interest rate can adjust every year up or down, depending on the market. These are good for people who don’t plan on living in their home very long and/or are looking for a lower interest rate and payment. I would STRONGLY advise against an adjustable mortgage now.

Fixed-rate mortgages are more traditional and offer a fixed interest rate (and thus a fixed monthly payment) for a longer period, usually 15 or 30 years, though they’re available in 20 or 25 year terms. These are good for people who like a predictable payment and plan on living in their home for a long time.

Both fixed and adjustable rate mortgages can have an interest-only payment. What this means is that for a certain amount of time during the loan term, you’re allowed to pay only enough to cover the interest portion of your payment. You can still pay principal when you wish, but don’t have to if your budget is tight. There is a myth that with interest-only mortgages, you don’t build equity. This is not necessarily true, since you can build equity through home appreciation. The benefit to interest-only mortgages is that you increase your cash flow by not paying principal.

3. Look at Homes

A quick search on our site https://www.homes4saleinri.com/ will bring up thousands of homes for sale. Educating yourself on your local market and working with an experienced REALTOR®, can help you narrow your priorities and make an informed decision about which home to choose. Good REALTORS® will ask you questions about what you want and need in a home and compare that with what you can afford. When you receive listings to consider, before scheduling an appointment drive by them to see if you like the neighborhood. The housing inventory is tight in southern New England, so don’t get frustrated if other buyers get an offer in before you, or they offer more money. That happens A LOT in this market.

4. Choose a Home

While no one can know for sure what will happen to housing values, if you choose to buy a home that meets your needs and priorities, you’ll be happy living in it for years to come. Once you and the seller have reached agreement on a price, the house will go into escrow, which is the time-period it takes to complete all of the remaining steps in the home buying process.

Don’t forget people make money in real estate when they buy it, NOT when they sell it. A good, experienced REALTOR® will help you determine the best “Value” for your situation.

5. Home Inspection

Typically, purchase offers are contingent on a home inspection of the property to check for signs of structural damage or things that may need fixing. Your real estate agent usually will help you arrange to have this inspection conducted within a few days of your offer being accepted by the seller. This contingency protects you by giving you a chance to renegotiate your offer or withdraw it without penalty if the inspection reveals significant material damage.

Remember, a Home Inspection is a “snapshot” of the condition of home on a specific day at aa specific time. Home inspectors typically don’t have access to 2/3’s of the home so they cannot be expected to inspect/observe conditions for areas they cannot see. They cannot see behind paneling, inside walls, or around boxes stacked up in a basement or garage.

You will receive a report on the home inspector’s findings. You can then decide if you want to ask the seller to fix anything on the property before closing the sale. Before the sale closes, you will have a walk-through of the house, which gives you the chance to confirm that any agreed-upon repairs have been made.

6. Funding

The cost of financing your home purchase is usually greater than the price of the home itself (after interest, closing costs, and taxes are added). Get as much information as possible regarding your mortgage options and other costs. Your Lender will take care of all of the financing details, paperwork, arrange the appraisal and keep you informed.

7. Make an Offer

While much attention is paid to the asking price of a home, a proposal to buy includes both the price and terms. In some cases, terms can represent thousands of dollars in additional value—or additional costs—for buyers.

8. Find Insurance

No homeowner should be without insurance. Real estate insurance protects owners in the event of catastrophe. If something goes wrong, insurance can be the bargain of a lifetime. Joe can recommend a good insurance agent who is experienced in working with home buyers – especially first time home buyers.

9. Movers

It is highly recommended that you use the services of a licensed, insured, experienced mover. Whether moving across town or across the country, utilize the services of a professional mover. The potential cost of moving yourself or with “amateur” movers can be significant. Damage to furniture, floors, walls, the cost of renting a truck, quilts, dollies, straps, etc, quickly add up. Then there is always the possibility of bodily injury; hurting your back or someone sustaining serious injury that could involve lawsuits.

The fees charged by a professional mover usually are less than the above potentialities.

The Moving Company by preferred Luca & Marano

10. The Closing

Before the Closing, the Buyer’s REALTOR® should arrange for a Final Walk-Through, of the house to confirm that all of the Seller’s belongings that should have been removed, and those that should remain are still in the house, and that no damage transpired overnight.

Preferred by Luca & Marano

The closing process, also known as “settlement” or “escrow,” is increasingly computerized and does vary in different areas. In practice, closings bring together a variety of parties (Buyer and Seller, Closing/Escrow Representative, and sometimes a Seller’s Closing Attorney) who are part of the real estate transaction.

10. Post Closing

Don’t forget to have the utilities, internet access, landline telephone service etc switched into your name. It is much easier to switch service while it is still “on” compared to after it has been terminated.

In 1963, Martin Luther King, Jr. inspired a powerful movement with his famous “I Have a Dream” speech. Through his passion and determination, he sparked interest, ambition, and courage in his audience. Today, reflecting on his message encourages many of us to think about our own dreams, goals, beliefs, and aspirations. For many Americans, one of those common goals is owning a home: a piece of land, a roof over our heads, and a place where we can grow and flourish.

If you’re dreaming of buying a home this year, start by connecting with a local real estate professional to understand what goes into the process. With a trusted advisor at your side, you can then begin to answer the questions below to set yourself up for homebuying success.

1. How Can I Better Understand the Process, and How Much Can I Afford?

The process of buying a home is not one to enter into lightly. You need to decide on key things like how long you plan on living in an area, school districts you prefer, what kind of commute works for you, and how much you can afford to spend.

Keep in mind, before you start the process to purchase a home, you’ll also need to apply for a mortgage. Lenders will evaluate several factors connected to your financial track record, one of which is your credit history. They’ll want to see how well you’ve been able to minimize past debts, so make sure you’ve been paying your student loans, credit cards, and car loans on time. If your financial situation has changed recently, be sure to discuss that with your lender as well. Most agents have loan officers they trust and will provide referrals for you.

“Financial planners recommend limiting the amount you spend on housing to 25 percent of your monthly budget.”

2. How Much Do I Need for a Down Payment?

In addition to knowing how much you can afford on a monthly mortgage payment, understanding how much you’ll need for a down payment is another critical step. Thankfully, there are many different options and resources in the market to potentially reduce the amount you may think you need to put down.

If you’re concerned about saving for a down payment, start small and be consistent. A little bit each month goes a long way. Jumpstart your savings by automatically adding a portion of your monthly paycheck into a separate savings account or house fund. AmericaSaves.orgsays:

“Over time, these automatic deposits add up. For example, $50 a month accumulates to $600 a year and $3,000 after five years, plus interest that has compounded.”

Before you know it, you’ll have enough for a down payment if you’re disciplined and thoughtful about your process.

3. Saving Takes Time: Practice Living on a Budget

As tempting as it is to pass the extra time you may be spending at home these days with a little retail therapy, putting that extra money toward your down payment will help accelerate your path to homeownership. It’s the little things that count, so start trying to live on a slightly tighter budget if you aren’t doing so already. A budget will allow you to save more for your down payment and help you pay down other debts to improve your credit score.

A survey of millennial spending shows, “68% reported that shelter in place orders helped them save for their down payment.” Danielle Hale, Chief Economist at realtor.com, also notes:

“If there is any silver lining to the current economic landscape, it’s that mortgage rates are hanging around record lows…Additionally, shelter-in-place orders helped many who were fortunate enough to keep their jobs save for a down payment — one of the largest hurdles of buying a home. The combination of low rates and the opportunity to save is enabling many millennials to move up their home buying timeline.”

While you don’t need to cut all of the extras out of your current lifestyle, making smarter choices and limiting your spending in areas where you can slim down will make a big difference.

Bottom Line

If homeownership is on your dream list this year, take a good look at what you can prioritize to help you get there. To determine the steps you should take to start the process, let’s connect today.