By Joe Luca, REALTOR®

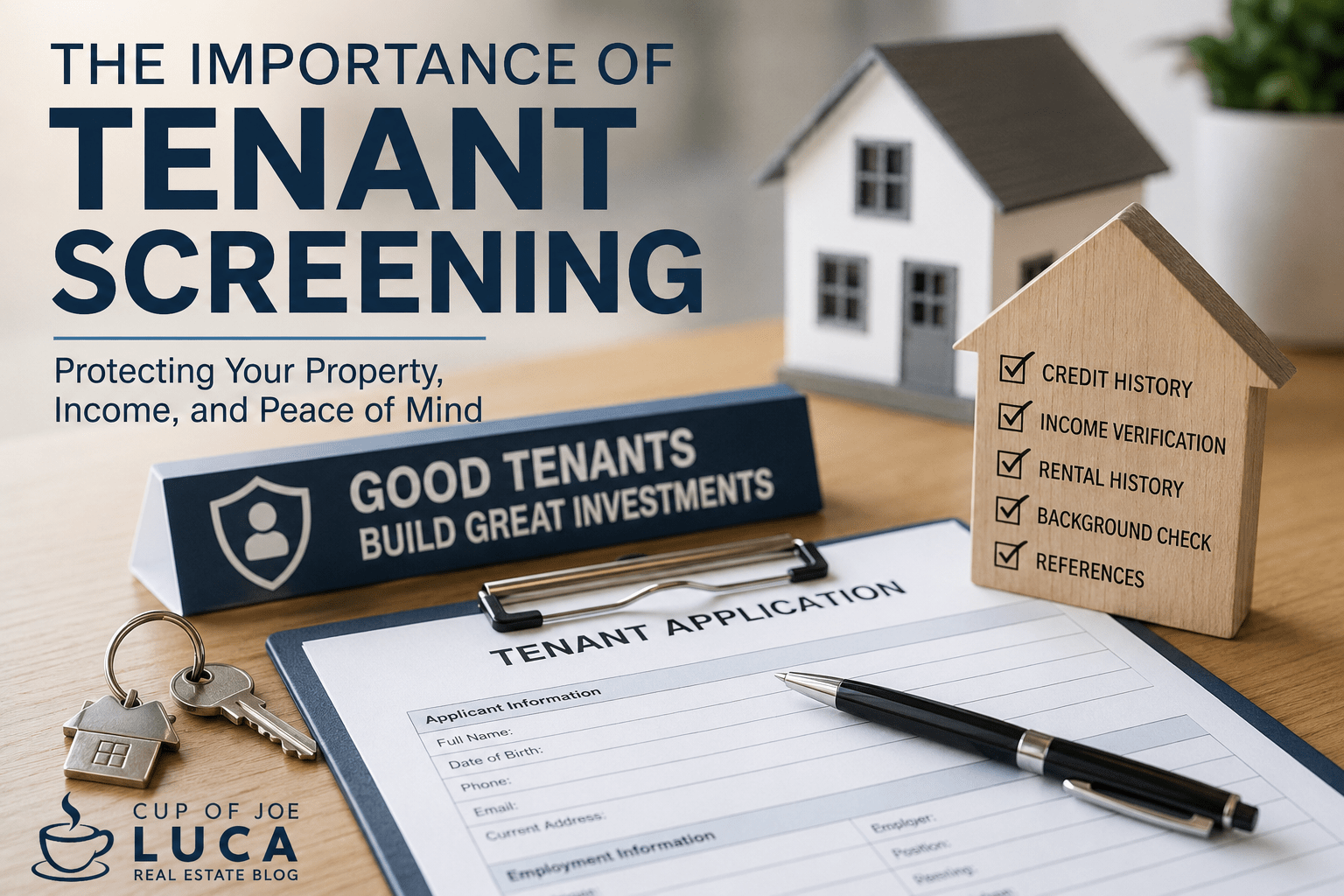

In today’s housing market, owning rental property can be one of the most effective ways to build long-term wealth, create additional income, and strengthen financial security. But one of the biggest mistakes a landlord can make is rushing through the tenant screening process because they are anxious to fill a vacancy quickly.

Whether you own a single-family rental home in Rhode Island, a multifamily property in Massachusetts, or you are thinking about becoming a first-time landlord, proper tenant screening is one of the most important risk-management tools available to property owners.

The reality is simple:

The wrong tenant can cost thousands of dollars in unpaid rent, legal fees, property damage, stress, and lost time.

At the same time, landlords must also remember that tenant screening must always comply with federal, state, and local Fair Housing laws. The goal is not to discriminate or make assumptions. The goal is to apply consistent, lawful, objective standards designed to protect both the landlord and the tenant.

Why Tenant Screening Is So Important

Many property owners focus almost entirely on monthly rent amounts. Experienced investors often focus more heavily on consistency, reliability, and risk reduction.

A tenant who pays on time, respects the property, communicates honestly, and intends to stay long term is often far more valuable than someone who simply offers the highest rent.

Good tenant screening can help reduce:

- Late payments

- Evictions

- Property damage

- Lease violations

- Neighbor complaints

- Turnover costs

- Legal disputes

- Vacancy losses

In many cases, one problematic tenancy can erase years of positive cash flow.

Tenant Screening Is About Patterns

A proper screening process is not about finding “perfect” tenants. Very few people have perfect credit, perfect income, or perfect life circumstances.

Instead, professional screening looks for patterns.

Questions landlords should evaluate include:

- Does the applicant have a history of paying obligations on time?

- Is their income stable and verifiable?

- Have they demonstrated responsibility in previous housing situations?

- Are there inconsistencies in the application?

- Do references and documentation align with the information provided?

Often, the biggest warning signs are not dramatic issues. They are inconsistencies, incomplete information, evasiveness, or rushed pressure tactics.

The Cost of Skipping Background Checks

Some landlords skip screening because they:

- Know the applicant personally

- Feel uncomfortable asking questions

- Want to avoid vacancy costs

- Believe “it will probably work out”

Unfortunately, informal decisions can create major financial exposure.

A comprehensive tenant screening process may include:

- Credit review

- Income verification

- Employment verification

- Rental history

- Reference checks

- Eviction history

- Criminal background checks where legally permitted

- Identity verification

The small upfront investment in screening can potentially save thousands later.

Fair Housing Compliance Is Critical

Every landlord should understand that tenant screening must comply with Fair Housing laws.

Federal law prohibits discrimination based on protected classes, and Rhode Island and Massachusetts may provide additional protections beyond federal law.

This means landlords should:

- Use consistent screening criteria

- Apply the same standards to every applicant

- Document decisions carefully

- Avoid subjective or emotional decision-making

- Focus on legitimate business-related factors

Consistency is one of the best protections for both landlords and tenants.

The Importance of Income Verification

One of the most common problems in rental housing today is income instability.

Many experienced landlords prefer tenants whose gross monthly income falls within a reasonable multiple of the monthly rent obligation. While standards vary, consistency matters more than arbitrary decisions.

Verification may include:

- Pay stubs

- W-2 forms

- Tax returns

- Bank statements

- Employer verification letters

- Self-employment documentation

In an era of AI-generated documents and online fraud, verification has become increasingly important.

Credit Scores Tell a Story — But Not the Entire Story

Credit history can provide valuable information, but it should rarely be the only factor considered.

A credit report may reveal:

- Payment history

- Collections

- Charge-offs

- Debt levels

- Bankruptcy filings

- Overall financial habits

However, experienced landlords also understand context matters.

A temporary hardship from a medical issue or divorce may be very different from a long-term pattern of financial irresponsibility.

The goal is not perfection. The goal is evaluating overall risk responsibly and legally.

Rental References Can Reveal Important Details

Previous landlords can often provide valuable insight into:

- Payment consistency

- Lease compliance

- Property condition

- Communication style

- Neighbor interactions

- Notice practices

However, landlords should also recognize that not every reference is equally reliable. Some landlords may avoid negative comments entirely for liability reasons, while others may simply want a difficult tenant to move elsewhere quickly.

This is why tenant screening works best when multiple factors are evaluated together.

The Eviction Process Is Expensive and Stressful

Many first-time landlords underestimate how costly and time-consuming evictions can become.

Potential costs may include:

- Lost rent

- Court costs

- Attorney fees

- Property repairs

- Vacancy periods

- Emotional stress

- Lost productivity

Even in situations where the landlord ultimately prevails, the financial damage can already be significant.

Proper screening dramatically reduces the likelihood of these situations.

Technology Has Changed Tenant Screening

Modern screening tools can provide:

- Online applications

- Automated background checks

- Digital identity verification

- Credit and eviction reporting

- Fraud detection systems

At the same time, landlords should avoid over-relying on automation alone.

Technology is helpful, but human judgment, consistency, documentation, and legal compliance still matter tremendously.

Small Landlords Need Screening the Most

Ironically, smaller landlords often skip screening more frequently than large institutional investors.

But smaller property owners typically have less financial margin for error.

A large corporation may survive several bad tenants.

A small landlord with one or two units may suffer major financial hardship from a single problematic lease.

That is why careful tenant screening is not merely a “best practice.”

It is a core financial protection strategy.

Final Thoughts

Tenant screening is not about being overly strict or unfair. It is about making responsible, informed, and legally compliant decisions that protect everyone involved in the rental relationship.

Good tenants deserve professional landlords.

Professional landlords should also protect their investment responsibly.

In today’s market, careful tenant screening may be one of the most important financial decisions a property owner makes.

Whether you are a first-time investor, an accidental landlord, or someone expanding a rental portfolio in Rhode Island or Massachusetts, taking the time to screen properly can help reduce stress, protect your property, and improve long-term financial outcomes.

Frequently Asked Questions About Tenant Screening

What is tenant screening?

Tenant screening is the process landlords use to evaluate rental applicants before approving a lease. This process may include reviewing credit, income, rental history, references, background information, and identity verification.

Why is tenant screening important?

Tenant screening is important because it helps reduce the risk of unpaid rent, property damage, evictions, and lease violations. A proper screening process can protect both the landlord’s financial investment and the overall rental experience.

Can landlords check a tenant’s credit report?

Yes, landlords can check a tenant’s credit report with the applicant’s written permission. Credit reports may help identify payment history, debt obligations, and financial patterns.

How much income should a tenant have to qualify?

Most landlords look for tenants whose income reasonably supports the monthly rent payment. Specific standards vary, but consistency and documentation are important.

Are landlords allowed to perform background checks?

Yes, landlords are generally allowed to perform background checks where permitted by law and with proper authorization. However, landlords must comply with Fair Housing laws and any applicable state or local regulations.

What are some red flags during tenant screening?

Common red flags include unverifiable income, inconsistent application information, prior evictions, repeated late payments, falsified documents, or incomplete applications. No single factor automatically disqualifies an applicant, but patterns matter.

Should landlords contact previous landlords?

Yes, contacting previous landlords can help verify rental history and identify patterns of behavior. Previous landlords may provide insight into payment habits, lease compliance, and property care.

Is tenant screening different in Rhode Island and Massachusetts?

Yes, tenant screening laws can vary between Rhode Island and Massachusetts. Landlords should always understand and comply with federal, state, and local housing regulations before making rental decisions.

Can a landlord deny an application?

Yes, landlords can deny an application if the decision is based on lawful, objective screening criteria applied consistently to all applicants. Decisions must comply with Fair Housing laws and applicable state regulations.

What is the biggest mistake landlords make during screening?

The biggest mistake many landlords make is rushing the screening process because they want to fill a vacancy quickly. Careful screening often helps prevent much larger financial and legal problems later.