If you’ve been dreaming of owning a home in Southern New England—think Connecticut’s charming towns, Rhode Island’s coastal gems, or the historic corners of southern Massachusetts—2025 might be your moment. As of March 11, 2025, the real estate market here is showing signs of opportunity for buyers. From economic shifts to local trends, here’s why now could be the perfect time to plant your roots in this picturesque region.

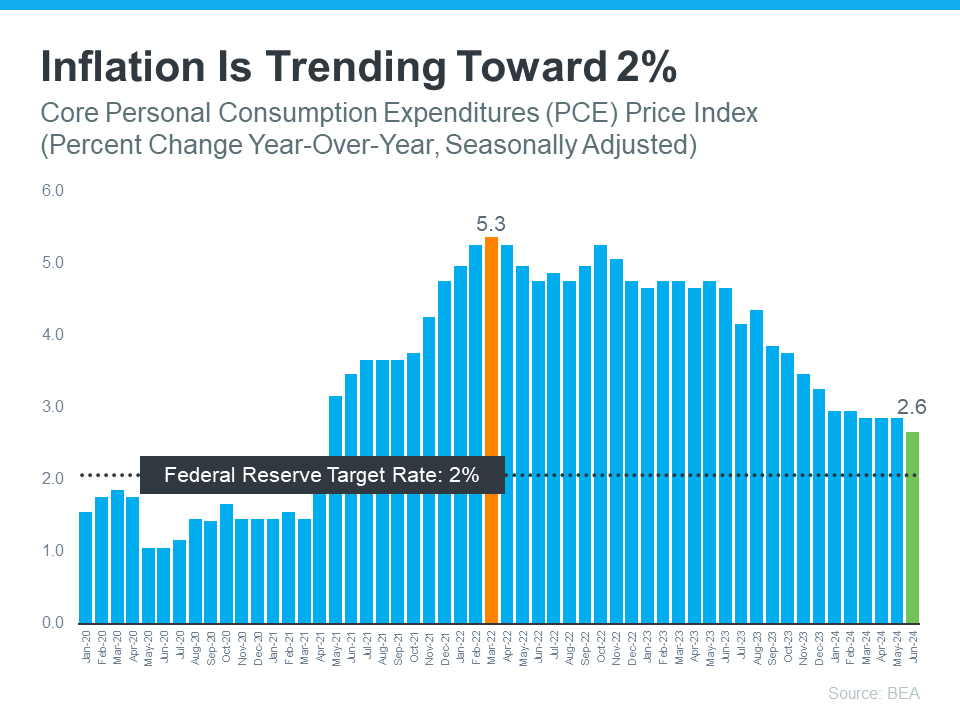

1. Interest Rates Are Settling Down

After a wild ride in recent years, mortgage rates appear to be stabilizing across the U.S., and Southern New England is no exception. While we’re not back to the rock-bottom rates of the 2010s, the steep climbs of the early 2020s have eased. For buyers in places like New Haven or Providence, this means more predictable mortgage payments and a chance to lock in a rate before any surprises. With the Federal Reserve keeping a close eye on inflation, rates could hold steady—giving you a solid window to finance that Cape Cod-style home or colonial fixer-upper.

2. Inventory Is Ticking Up Across the Region

Southern New England has felt the inventory crunch hard, with sellers clinging to their low-rate mortgages or waiting out peak prices. But early 2025 is bringing a shift. In towns like Mystic, CT, or Bristol, RI, more “For Sale” signs are popping up. Maybe it’s empty nesters downsizing, retirees heading south, or homeowners feeling the market has topped out. Whatever the reason, this uptick means more choices—whether you’re eyeing a waterfront cottage in Narragansett or a suburban spread in West Hartford. More options also mean less cutthroat bidding wars, a welcome relief for buyers.

3. Prices Are Softening in Hotspots

The pandemic boom sent prices soaring in Southern New England, especially in desirable spots like Fairfield County or the South Shore of Massachusetts. But as demand normalizes, some of these overheated markets are cooling. Sellers who bought at the 2021 peak might be more open to negotiation, especially in areas where listings are lingering a bit longer. In places like Cranston, RI, or Milford, CT, you could snag a deal that feels more reasonable than it did two years ago. It’s not a buyer’s market everywhere, but the balance is tipping your way in many towns.

4. Southern New England’s Long-Term Appeal Holds Strong

This region’s charm—historic villages, top-notch schools, and proximity to both Boston and New York—makes it a perennial winner for real estate investment. Even with short-term ebbs and flows, home values here tend to climb over time. Buying now in, say, Portsmouth, RI, or Simsbury, CT, sets you up for equity growth as hybrid work trends keep the area attractive to professionals and families alike. A home purchased in 2025 could be your family’s cornerstone—and a financial win—by 2035.

5. Local Incentives Are Sweetening the Deal

From builders in growing suburbs like Plainfield, CT, to sellers in competitive markets like Attleboro, MA, incentives are emerging. New developments might offer rate buydowns or closing cost help, while individual sellers could throw in extras—like covering roof repairs or offering flexible move-in dates—to close the deal. These perks can shave thousands off your upfront costs, making homeownership more attainable in a region where prices can still feel steep.

6. Seasonal Timing Works in Your Favor

March in Southern New England is a quiet season for real estate. The spring rush hasn’t fully kicked in, and winter’s chill keeps some buyers indoors. That means less competition as you tour that farmhouse in Litchfield County or that bungalow in Westerly, RI. Sellers listing now might be extra motivated—perhaps they’re relocating for work or eager to sell before the summer crowd arrives. It’s a strategic moment to strike while the market’s still waking up.

A Word of Caution

Southern New England’s market varies widely—Greenwich, CT, is a different beast from Fall River, MA. Check local trends, get pre-approved, and team up with a realtor who knows the area inside out. Coastal properties might still carry flood insurance costs, and older homes could need TLC. But for those ready to navigate these quirks, the rewards are there.

The Bottom Line

March 2025 is shaping up as a buyer’s sweet spot in Southern New England. With steadier rates, growing inventory, softening prices in key areas, and the region’s enduring appeal, the stars are aligning. So, grab your map, hit the open houses—from Stamford to Stonington—and make your move. That quintessential New England home, complete with a front porch and autumn leaves, might be waiting for you right now.

If you have any questions, or would like to connect, email me: Joe@JoeLucacaRealtor.com